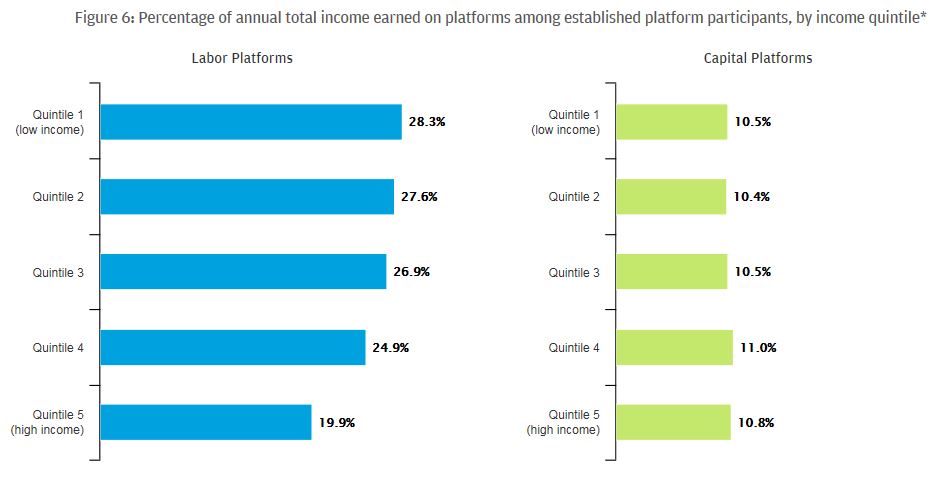

In the JPMorgan Chase Institute's report Paychecks, Paydays, and the Online Platform Economy, we documented that 4 percent of adults earned income from the Online Platform Economy between October 2012 and September 2015. Despite the tremendous growth in participation in the Online Platform Economy—a 47-fold increase over three years—these online "gigs" remained a secondary source of income for most people. In months when individuals earned platform income, labor platforms, such as Uber or TaskRabbit where individuals perform discrete tasks or assignments, contributed 33 percent of total monthly income, and capital platforms, such as eBay or Airbnb where individuals sell goods or rent assets, contributed 20 percent of total monthly income.

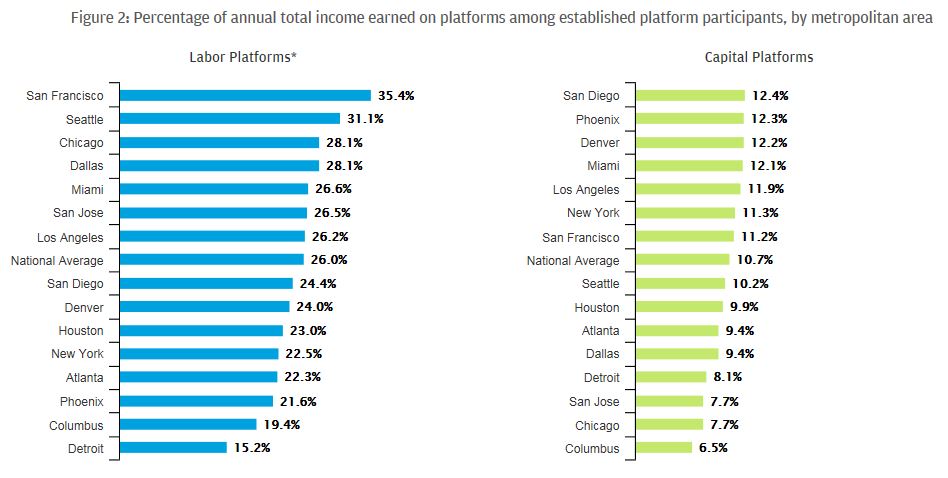

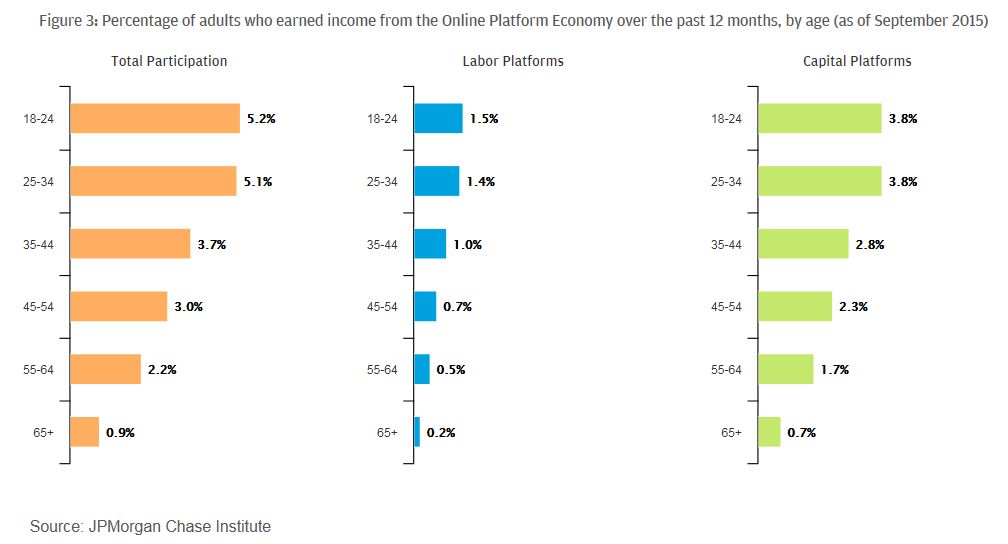

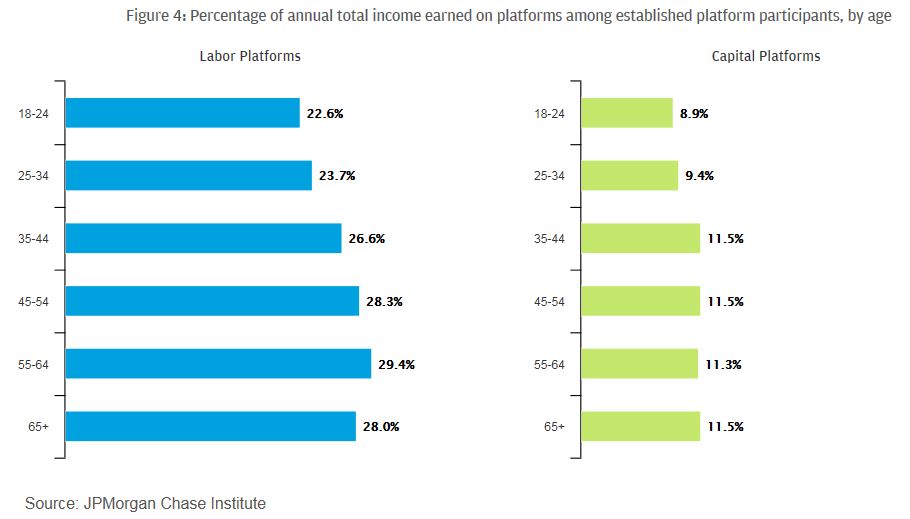

With many policy debates underway, including whether platform workers should constitute a new class of "independent workers" and how to provide traditional workplace benefits for them, it is important to understand who would be most affected by proposed policies or the results of class action lawsuits. We find that the Online Platform Economy contributed significantly to the bottom line for certain segments of the population, notably labor platform participants in general, and specifically labor platform earners who live in San Francisco, or who are 35 and older or have low-to-moderate incomes. Among these segments, platform earnings represented, on average, more than a fourth of their income over a 12-month span.

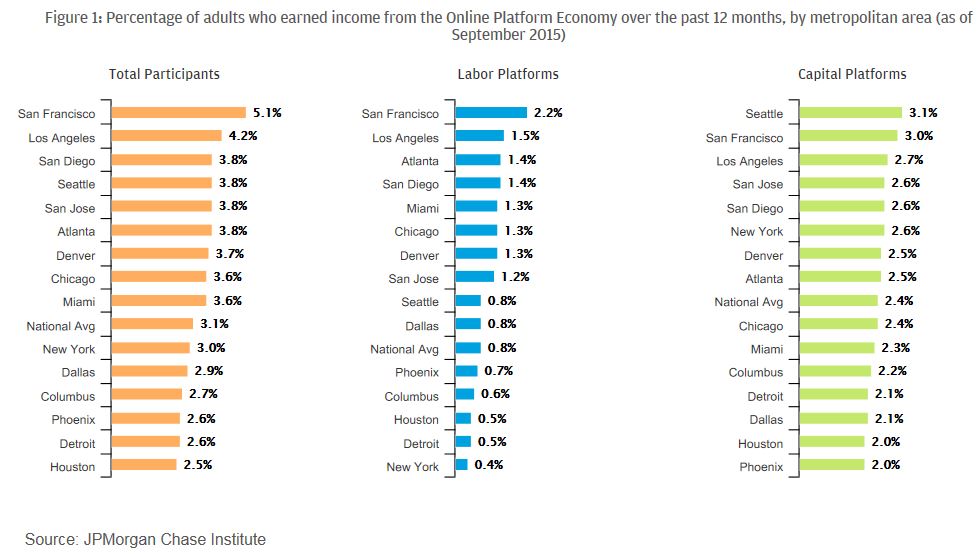

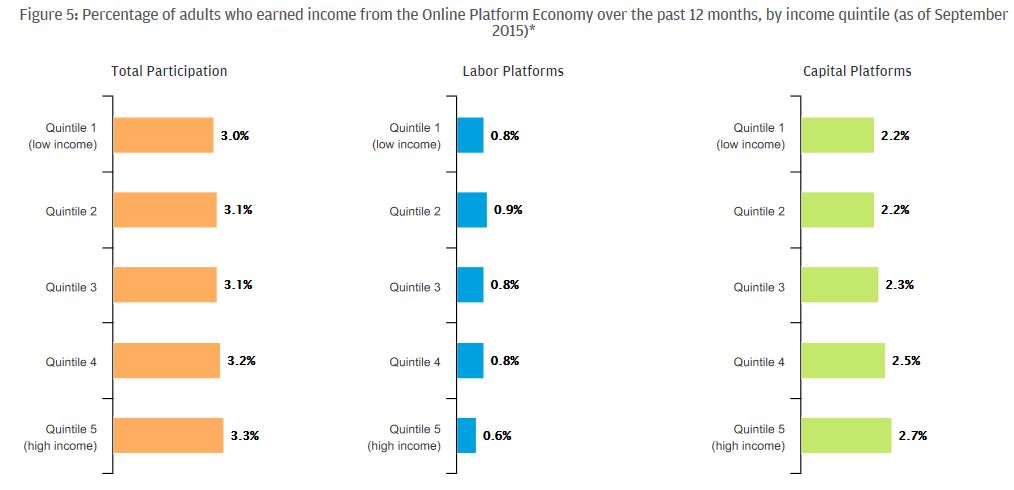

To shed light on who earns the most from online platforms, we drew on our anonymized sample of over 260,000 core Chase checking account customers who earned income on at least one of 30 platforms—the largest sample of platform earners analyzed to date. Here we focus on the 196,000 individuals who participated over the twelve month period between October 2014 and September 2015. During this span, 3.1 percent of adults earned income from online platforms, 2.4 percent in capital platforms and 0.8 percent in labor platforms.

1. West Coast cities are the epicenter of the Online Platform Economy, with San Francisco topping the charts for both participation in and reliance on online labor "gigs."

In San Francisco, where many of the largest online platform companies are headquartered, 5.1 percent of adults earned income from platforms over the twelve month period ending September 2015, compared to 3.1 percent nationally (Figure 1). While San Francisco had the highest participation rate for labor platforms, Seattle had the highest participation rate for capital platforms. Across all metropolitan areas more people earned income from capital platforms than labor platforms, and very few people—less than 3 percent of participants—earned income from both labor and capital platforms.

There is wide dispersion in the rates of participation in labor platforms across the 15 cities in Figure 1. Participation in labor platforms ranged from a high of 2.2 percent in San Francisco to a low of 0.4 percent of adults in New York City—a five-fold difference. A number of factors likely contributed to this dispersion, including the timing of when platform companies entered each market, regulatory efforts in response to their growth, and local labor market and price conditions. In contrast to labor platforms, there was less variation in the rate of participation in capital platforms across cities—participation rates ranged from a high of 3.1 percent in Seattle to a low of 2.0 percent in Houston and Phoenix.