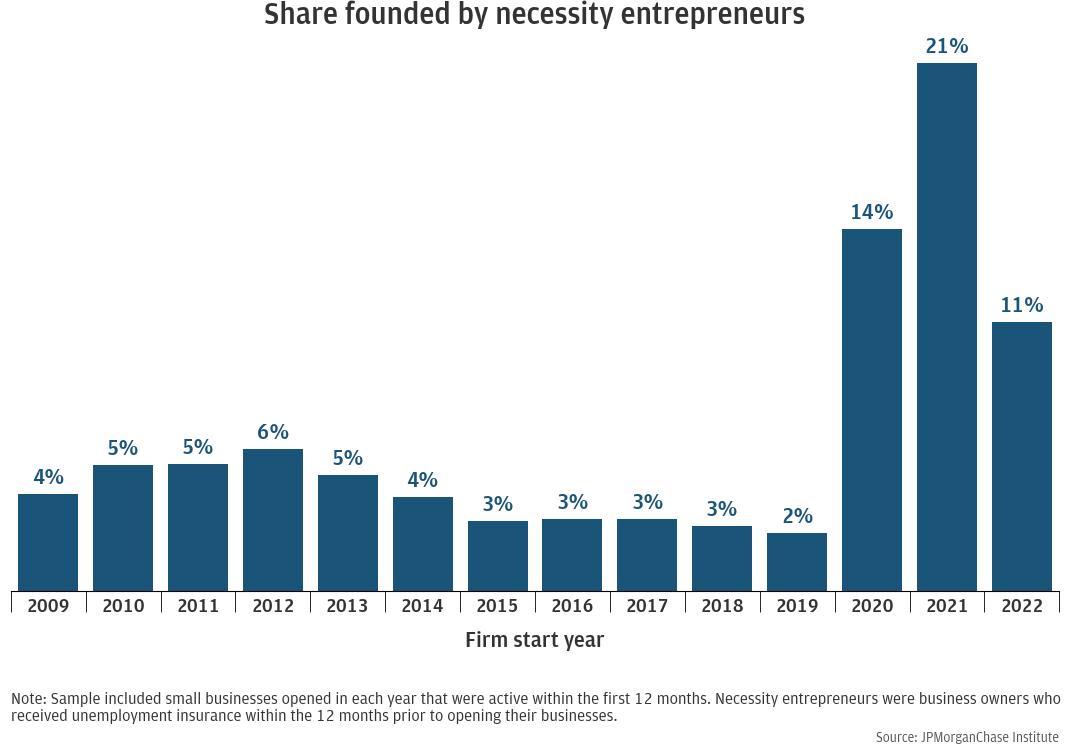

Figure 1: Necessity entrepreneurs started a larger share of new firms during economic downturn.

Latest news

An Ohio-based company is protecting first responders around the world

With support from JPMorganChase, Fire-Dex is providing protective equipment to firefighters in 100 countries and all 50 states.

Learn moreLatest news

Veteran’s Unconventional Path to Landing her Dream Job in Tech

U.S. Army Veteran Ashley Wigfall transitioned to a civilian role and charted her path to technologist through mentorship and skills training at the JPMorgan Chase tech hub in Plano, Texas.

Learn more

Research

October 29, 2024

After a decades-long downward trend in business dynamism, a surge in new business applications during the COVID-19 pandemic stirred cautious optimism for future economic growth (Decker, et al. 2016; Decker and Haltiwanger 2022). Over 545,000 new business applications were filed in July 2020, nearly twice the level 12 months earlier.1 That momentum continued even as pandemic restrictions abated, and business applications have remained elevated through the first quarter of 2024, relative to pre-pandemic trends.

Unpacking these dynamics can help policymakers better understand the relationship between recent entrepreneurial activity and future economic growth. Entrepreneurs founding new businesses during the past few years did so under unique economic and labor market conditions, which may have affected their prospects and outcomes. In strong economies, new businesses may form to take advantage of the opportunity created by robust demand. In downturns, new businesses may form as the labor market weakens and some workers turn to self-employment, perhaps out of necessity. These necessity entrepreneurs may face challenges in growing their businesses. When a larger share of new firms is founded by necessity entrepreneurs, the trajectory of subsequent aggregate economic growth may be muted.

In this report, we focused on one type of necessity entrepreneurs, ones that started a business after involuntary unemployment. We analyzed firms started by both necessity and opportunity entrepreneurs in different economic conditions over 14 years, a period that includes two recessions. Our unique data asset provides the basis for our distinctive contribution in not only identifying necessity entrepreneurs but also studying their financial outcomes. In particular, we found:

Our findings may also have implications for other types of necessity entrepreneurship. To the extent that those who are disadvantaged in traditional labor markets—such as unemployed workers, recent immigrants, or returning citizens—may be more likely to start a business out of necessity, self-employment may not necessarily be an option that leads to financial security and building wealth. Consequently, entrepreneurship may have a limited role in reducing inequality in financial outcomes.

In an accompanying report, we found that although women were not more likely to be necessity entrepreneurs, the gender revenue gap persists among both necessity and opportunity entrepreneurs.

Nevertheless, entrepreneurship does play a role in both business dynamism and labor market fluidity. Policies that support self-employment as a viable option for both necessity and opportunity entrepreneurs can contribute to a dynamic economy. Policymakers and decision makers can use this report’s insights to inform expectations about economic growth, tailor small business programs to the objectives and circumstances of their founders, and support entrepreneurship as part of a well-functioning labor market.

We designed our research sample to compare the characteristics and financial performance of firms founded by necessity and opportunity entrepreneurs in different economic conditions. It does so by leveraging granular, longitudinal data from linked business and personal deposit accounts between 2009 and 2023, a period that includes two recessions.

As in much of our small business research, the de-identified firms in our sample all have Chase Business Banking deposit accounts that meet our criteria for being active and small. Given our focus on the initial years after founding, we required evidence of some activity during the first 12 months after the account opened. See the Appendix for details on the required activity. By construction, all firms in our sample survived at least one year. We further restricted the firms in our sample to ones where at least one owner had a personal deposit account in the 12 months before the business account and used transactions in these accounts to classify business owners as either necessity or opportunity entrepreneurs. See Box 1 for details.

Our unique data asset provides a large sample of over 880,000 firms founded by necessity and opportunity entrepreneurs over 14 years, during a period with varying economic conditions. Requiring business owners to have personal accounts in the year2 before opening their business accounts restricts the sample and may introduce selection bias if entrepreneurs who use the same bank for personal and business purposes are different from those who do not. However, median revenues and exit rates for this sample are similar to those in prior analytical samples (e.g., Farrell, Wheat, and Mac 2018) that employed fewer requirements, suggesting that this sample has similar properties as our larger, less restrictive samples.

Entrepreneurs may be motivated to start a business by a variety of reasons. Some may have ideas for new products or services they want to introduce. They may want to work for themselves or seek greater flexibility over their schedules. Others may prefer wage employment but are unable to find a suitable job. These reasons are neither exhaustive nor mutually exclusive, but they illustrate the range of motives that entrepreneurs have, which may in turn affect the kinds of businesses they start and their goals for those businesses.

Many researchers have used the framework of contrasting “opportunity” entrepreneurs who pursue business opportunities and “necessity” entrepreneurs who may have fewer options in the labor market.3 With our administrative data asset, we cannot discern the motives of business owners. However, we can use a proxy to identify one type of necessity entrepreneurs: workers who became involuntarily unemployed and later started a business.

Our data asset consists of firms with Chase Business Banking deposit accounts. We also restricted the dataset to the over 880,000 firms with at least one owner who had a personal Chase deposit account that was open in the 12 months preceding the opening of the business account. If we saw direct deposits of unemployment insurance4 (UI) in the personal account during the year before the business account opened, the firm was classified as founded by a necessity entrepreneur. Otherwise, the business owner was considered an opportunity entrepreneur.

An advantage of this methodology is that it applies the relatively objective criteria of UI receipt to a large sample of administrative data. Workers typically do not qualify for unemployment insurance if they quit, so our definition of necessity entrepreneurs includes those who were engaged in wage employment and involuntarily lost their jobs in the year before starting a new business.5 This suggests that they may have continued in wage employment if they could.

Our definition is consistent with but more stringent than Fairlie and Fossen’s proposal of using unemployment status prior to starting a business to identify necessity entrepreneurs (2019). Our methodology may miss some necessity entrepreneurs either because we did not observe their UI benefits, or they did not qualify for benefits. For example, UI payments may have been direct deposited into another non-Chase account, or they may have been distributed using prepaid debit cards or paper checks.6 Other necessity entrepreneurs may have been unemployed (i.e., without a job and searching for wage employment) but did not receive UI benefits within a year prior to starting a business. While our set of opportunity entrepreneurs likely includes some necessity entrepreneurs, we are confident that our sample of necessity entrepreneurs is identifying a relevant set of those who started a business within a year of involuntary unemployment.

While there are many reasons that might drive an entrepreneur to start a business, two macroeconomic drivers are especially salient—aggregate demand and labor market conditions. When favorable business conditions generate strong demand for their products and services, entrepreneurs may take advantage of the opportunity by starting new businesses (Schweitzer and Shane 2016). When labor markets are weak, workers may turn to self-employment and start new businesses out of necessity (Fairlie 2013). Notably, favorable business conditions and weak labor markets typically occur at opposite ends of the business cycle, causing the net effect of business cycles on aggregate new firm formation to be ambiguous.

Recent history provides two examples of economic downturns: the Great Recession and the COVID-19 pandemic. The share of firms that are new, which had declined since the 1980s, declined further during the Great Recession (Decker, et al. 2016). However, the national rate of new entrepreneurs, reported by the Kauffman Foundation,7 increased slightly in 2009-2010 and 2020-2021, coinciding with the downturns. Business applications8 decreased slightly during the Great Recession and at the onset of the COVID-19 pandemic only to increase markedly to over 545,000 in July 2020 (compared to about 280,000 in July 2019) and remained over 400,000 per month through the first quarter of 2024.9 Applications by likely employer businesses also increased during the pandemic and remained elevated through 2023, suggesting that the recent surge in applications was not only due to necessity entrepreneurs (Fikri and Newman 2024).

Regardless of the overall effect of economic conditions on total business formations, we might expect the share of new firms founded by necessity entrepreneurs—those that start businesses when they are unable to find suitable wage employment—to increase during periods of economic distress, consistent with the hypothesis that weak labor market conditions steer more workers toward self-employment. See Box 1 for a description of how we identified necessity entrepreneurs in our sample.

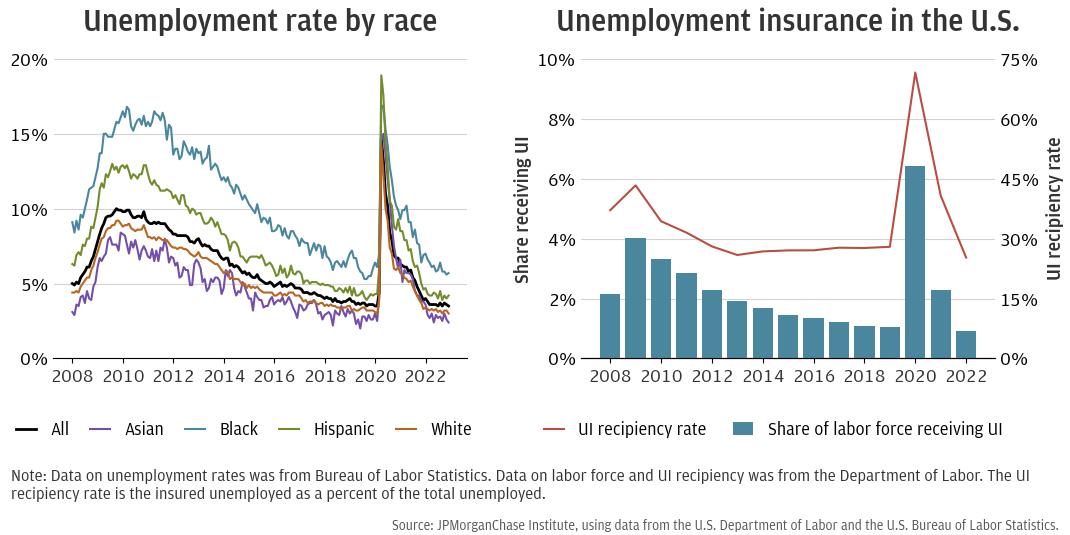

Figure 1 shows the share of firms in our sample founded by necessity entrepreneurs increased around the Great Recession and the COVID-19 pandemic. The highest share occurred in 2021, when 21 percent of firms founded had owners that received UI in the 12 months prior to the firm’s start. The increased share of necessity entrepreneurs in 2021 reflected the UI received in 2020-2021 and the pandemic recession from February 2020 to April 2020.10 Although the 2020 recession was short-lived, the determination of the economic trough was not made until July 2021.11 During the pandemic, the unemployment rate and share of the labor force receiving UI peaked during 2020 and remained elevated in 2021, as shown in Figure 2.

The businesses started around the Great Recession also showed a higher share founded by necessity entrepreneurs. While this recession lasted from December 2007 to June 2009, the peak was not determined until December 2008,12 and the trough was not determined until September 2010.13 Although the unemployment rate began to trend downward in April 2010, sharper declines did not begin until January 2012, when the unemployment rate was 8.3 percent, falling to 4.9 percent in January 2016 (Cunningham 2018). This longer tail of elevated unemployment rates is reflected in our sample: 4 to 6 percent firms of started in 2009 through 2014 were founded by necessity entrepreneurs, compared to 2 to 3 percent of those started between 2015 and 2019.

Figure 2 shows the national unemployment rate by race as well as measures of UI incidence between 2008 and 2022. The left panel shows how the unemployment rate declined gradually after the Great Recession. In comparison, the unemployment rate increased sharply in 2020 and subsided nearly as quickly. On the right panel of Figure 2, we calculated the share of the labor force receiving UI based on the U.S. Department of Labor’s estimates for the labor force and UI recipients. This share is lower than the unemployment rate, as not all unemployed persons receive UI. However, the share receiving UI is somewhat elevated after the end of the Great Recession, and a larger share of the labor force received UI in 2020 than in the Great Recession, a pattern that is reflected in our sample. The right panel also shows the UI recipiency rate, estimated as the insured unemployed as a percent of the total unemployed, which also suggests that there were more recipients during the pandemic recession than in the Great Recession.14

Our sample is also consistent with other estimates using different data sources. Using the Current Population Survey, the Kauffman Foundation found lower shares of opportunity entrepreneurs between 2009 and 2011 (about 74 percent), as well as in 2020 (nearly 70 percent), compared to nearly 87 in 2019.15 Lower shares of opportunity entrepreneurs imply higher shares of necessity entrepreneurs.

During economic downturns, labor market conditions are often unfavorable. The unemployment rate may rise as job seekers have more difficulty finding openings and layoffs increase the number of unemployed. Some may turn to self-employment as an alternative to wage employment. Consequently, necessity entrepreneurship increases during downturns. The founders’ circumstances as well as the macroeconomic environment may shape not only the types of firms founded but also their financial outcomes.

The sharp increase in business applications as well as uncertain economic conditions starting in 2020 suggest that the types of firms founded during this period may differ from past cohorts. In particular, the number of applications for non-store retailers rose sharply (Decker and Haltiwanger 2022). This increase may reflect the relatively low barriers to entry to start a non-store retailer as well as shifting consumer preferences away from in-person shopping (Wheat, et al. 2021).

Necessity entrepreneurs may face additional challenges in starting a business, which may make it more difficult for them to start firms in industries that require larger amounts of capital. More than 75 percent of small business owners in 2022 used personal savings or funds from friends and family as sources of capital when starting their firms (Misera and Perlmeter 2023). Having experienced recent unemployment, necessity entrepreneurs may have depleted some of their personal savings. During periods of economic distress, both necessity and opportunity entrepreneurs may find it more difficult to raise funds from friends and family.

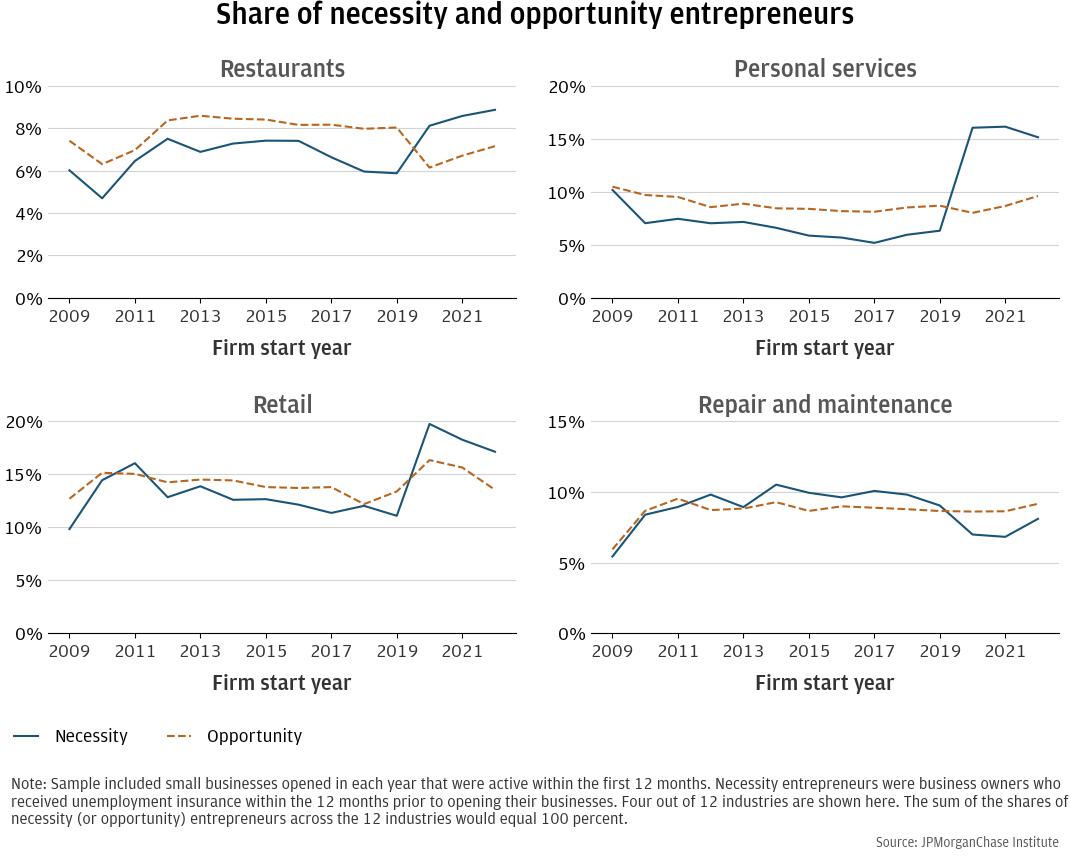

Here, we focused on four industries with sizable shares of necessity entrepreneurs. Since opportunity entrepreneurs comprised most of the sample, their industry shares can be interpreted as the general trend for new firms over time. The trend among necessity entrepreneurs provides a contrast, and divergences can provide insights about how their firms differ from those founded by opportunity entrepreneurs.

Figure 3 shows the share of both necessity and opportunity entrepreneurs in the restaurant, personal services, retail, and repair and maintenance industries. Notably, the share of necessity entrepreneurs in three of these industries—restaurants, personal services, and repair and maintenance—increased sharply in 2020 at the onset of the COVID pandemic. In each of these cases, the share of necessity entrepreneurs was lower than the share of opportunity entrepreneurs prior to 2020, but higher afterwards.

Two of the hardest hit industries during the pandemic were restaurants and personal services (Farrell, Wheat, and Mac 2020a), and yet the share of necessity entrepreneurs starting firms in these industries increased in 2020, despite the challenges that these industries faced at the time. This could reflect the higher unemployment rates in these industries during the pandemic and preferences among necessity entrepreneurs to start businesses in industries where they had work experience.

The unemployment rate for the restaurant industry was over 35 percent in April 2020 and was not consistently below 10 percent until the second half of 2021.16 The unemployment rate in personal services was over 47 percent in April 2020, although it decreased to about 10 percent by the end of the year.17 During this time, the share of opportunity entrepreneurs starting firms in the restaurant industry fell while the share in personal services remained similar to prior years.

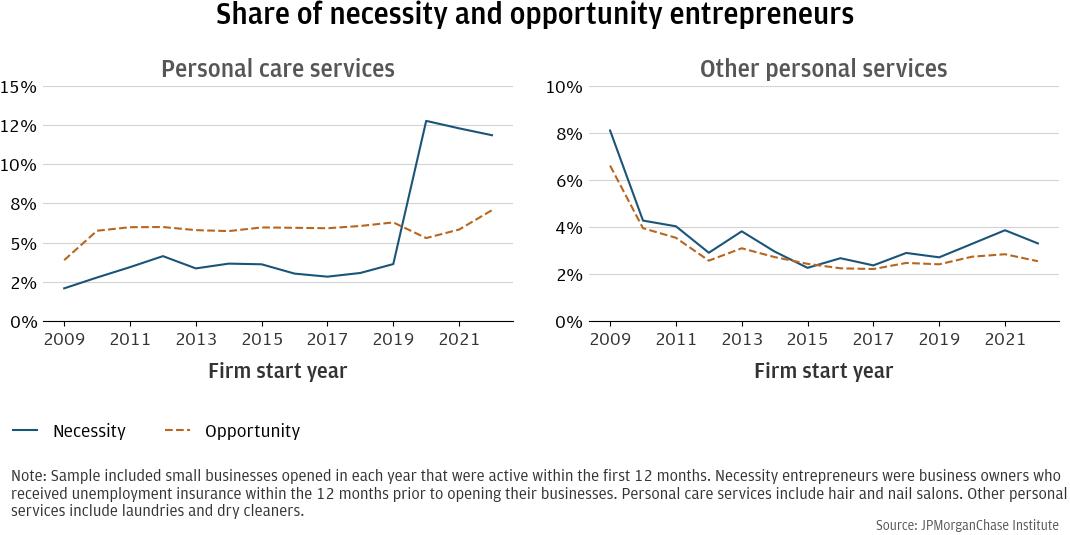

Sub-industry analysis reveals additional insights about the differences between firms founded by necessity and opportunity entrepreneurs. Within the personal services industry, the share of necessity entrepreneurs in personal care services (e.g., hair and nail salons) increased materially during the pandemic while the share in other personal services (e.g., dry cleaning and laundry) was relatively flat. Among opportunity entrepreneurs, there was little change in the share in either personal care or other personal services. The increasing share of all personal service firms was driven by increases in personal care services, despite the challenges in that sub-industry during the pandemic (Farrell, Wheat, and Mac 2020b). High unemployment rates in personal services may have led to larger shares of unemployed workers in this field turning to self-employment in similar roles.

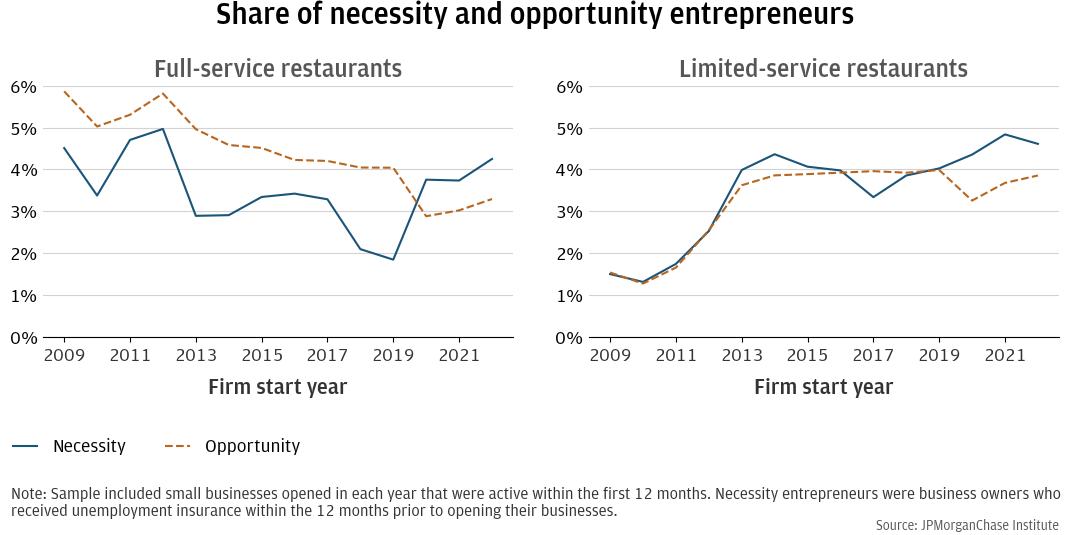

A similar dynamic may have been relevant among different types of restaurants, as shown in Figure 5. Among necessity entrepreneurs, the share of new firms as either full-service or limited-service restaurants increased during the pandemic. In contrast, the share of opportunity entrepreneurs opening new restaurants declined in 2020, likely reflecting the challenges of operating restaurants during the pandemic.

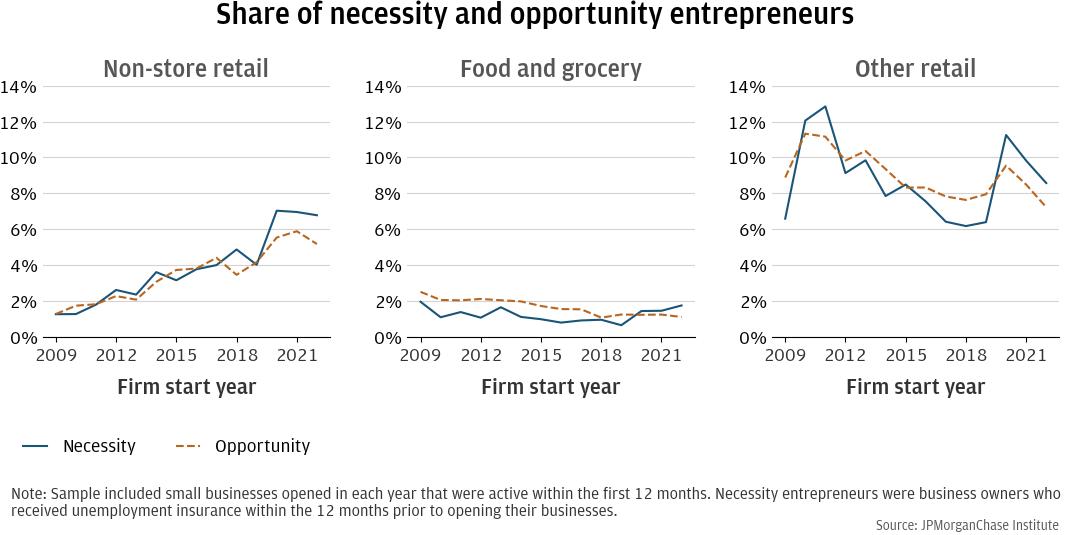

During the pandemic, grocery stores experienced strong outcomes relative to other types of retail (Farrell, Wheat, and Mac 2020b). However, grocery stores represented a small share of new firms. Consistent with business applications (Decker and Haltiwanger 2022), an increasing share of new firms founded by either necessity or opportunity entrepreneurs were non-store retailers,18 as shown in Figure 6, although that share had already been increasing over time. Overall, a larger share of necessity entrepreneurs during the pandemic started retail businesses compared to opportunity entrepreneurs, and that was true in each retail sub-industry.

During periods of economic distress, a larger share of new firms is founded by necessity entrepreneurs, and the types of firms differ from those of opportunity entrepreneurs. Despite the challenges faced by firms in the personal services and restaurant industries during the pandemic, unemployed workers founded increasing shares of businesses in these industries. They may have had relevant work experience in these industries, predisposing them to seek self-employment in the same industries. While these new ventures may benefit from their founders’ past work histories, industry-wide pressures may hamper their survival and growth.

Necessity and opportunity entrepreneurs have often concentrated in different industries, with some more pronounced contrasts during the pandemic, possibly due to the disproportionate effect of the pandemic on some industries, such as restaurants and personal services. Analogously, economic downturns can affect some demographic groups more severely than others, which can have implications on the population of necessity and opportunity entrepreneurs.

During economic downturns, younger workers often experience higher unemployment rates. During the pandemic, the unemployment rate for men aged 20 to 24 peaked at over 23 percent, compared to a peak of over 12 percent for men aged 55 and older (Falk, et al. 2021). Similarly, the peak unemployment rates around the Great Recession were over 19 percent for those aged 16 to 24 (in April 2010), and over 7 percent (in August 2010) for those aged 55 and older (Cunningham 2018).

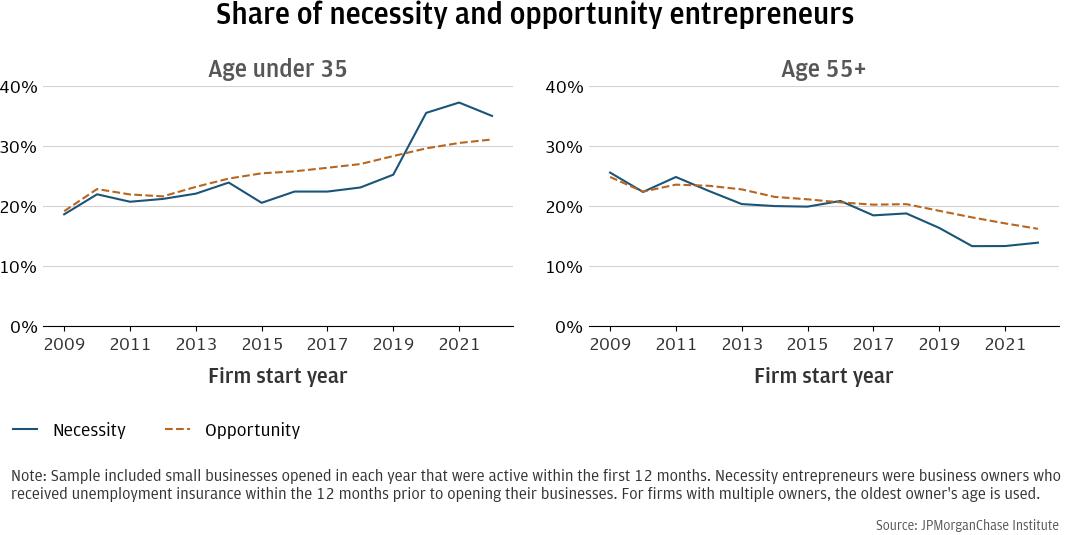

Higher unemployment rates among younger workers need not imply that necessity entrepreneurs are necessarily younger than opportunity entrepreneurs. For example, unemployed younger workers may have lower propensities to start businesses relative to their older counterparts. Figure 7 shows the share of necessity and opportunity entrepreneurs who were under age 35 as well as those aged 55 and over. For new firms between 2009 and 2019, which includes those started in the Great Recession, a slightly smaller share of necessity entrepreneurs was under 35, compared to the share in that age group for opportunity entrepreneurs. During the pandemic, the share of necessity entrepreneurs who were under 35 increased markedly. Among firms founded by opportunity entrepreneurs, the share of founders under age 35 also trended up over the years, but the increase during the pandemic was not as sharp. One potential explanation might be the supplemental unemployment insurance payments available during the pandemic,19 which could have provided younger workers with seed money with which to start their businesses.

Our sample distribution differs from the implications of other studies using different data sources. For example, using the Current Population Survey, Fairlie (2022) found the rate of new entrepreneurs to be the lowest among those aged 20 to 34.20 The Kauffman Foundation (2022) showed about 25 percent of new entrepreneurs in the 20-34 age group during 2009-2021, with 26 percent in 2021. The study showed a similar share for entrepreneurs aged 55-64, comprising nearly 23 percent in 2021.

While our sample shares are similar for the period 2009 to 2015, our upward trend in the share of younger entrepreneurs suggests some underlying differences. These differences may be related to basing our sample on the Chase retail banking footprint, which is more concentrated in urban areas, as well as requiring Chase personal deposit accounts in the year prior to establishing a business banking account. Nevertheless, the increasing share of necessity entrepreneurs under age 35 during the pandemic is worth noting.

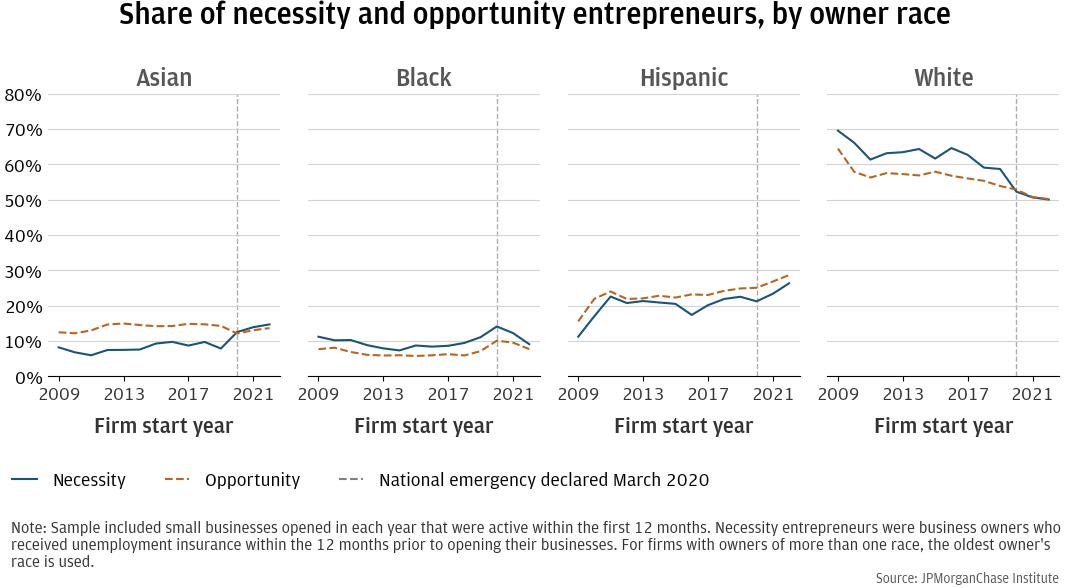

In our sample, we also found a declining share of necessity entrepreneurs who were White during the pandemic. Before the pandemic, more than 60 percent of necessity entrepreneurs were White; this share declined to about 50 percent during the pandemic. The shares of businesses founded by Asian and Hispanic necessity entrepreneurs increased during the pandemic, while the share founded by Black necessity entrepreneurs declined. That may appear inconsistent with the high unemployment rates experienced by Black workers, shown in Figure 2.

However, other studies have documented lower unemployment insurance recipiency among Black workers despite higher unemployment rates (Nichols and Simms 2012). Since our sample is based on observed receipt of unemployment insurance, our sample may be reflecting this underrepresentation of Black workers with unemployment insurance. Differing propensities to start a business may be another confounding factor.

As with our industry analysis in Finding 1, comparing shares of necessity entrepreneurs with corresponding opportunity entrepreneurs provides additional insights of historical trends. For example, in most years, over 60 percent of necessity entrepreneurs were White compared to less than 60 percent of opportunity entrepreneurs who were White, although these shares converged during the pandemic. Similarly, larger shares of necessity entrepreneurs were Black, compared to the shares of opportunity entrepreneurs who were Black.

The reverse was observed for Asian and Hispanic business owners. About 15 percent of opportunity entrepreneurs were Asian, compared to 10 percent necessity entrepreneurs prior to the pandemic. This pattern ended in 2020, when the share of Asian necessity entrepreneurs increased. The share of opportunity entrepreneurs who were Hispanic was also consistently higher than their corresponding share of necessity entrepreneurs.

The demographic composition of necessity and opportunity entrepreneurs over time has been a function of unemployment rates as well as propensity and resources to start a business. The sharp increase in unemployment during the pandemic, coupled with higher UI recipiency rates as well as supplemental UI payments, may have affected the constitution of necessity entrepreneurs in recent years. Since the pandemic, a larger share of necessity entrepreneurs has been under age 35 and non-White.

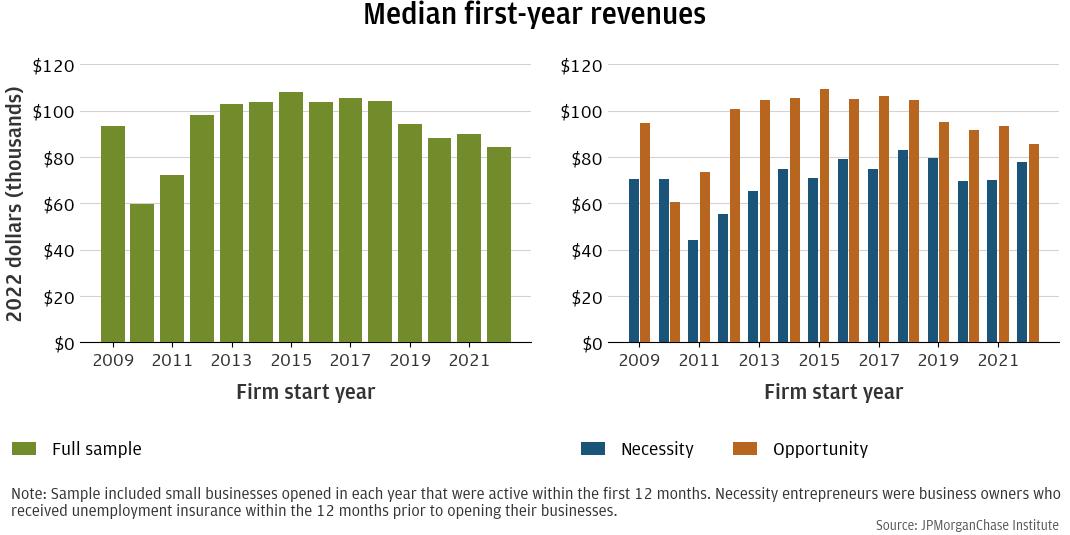

Starting a new business can be challenging in the best of times. Not surprisingly, businesses founded during periods of economic distress have lower initial revenues. Figure 9 shows the median first-year revenues for firms started between 2009 and 2022. The left panel shows the median for all firms founded in each year, inflation-adjusted to 2022 dollars. Firms founded during and after the Great Recession and during the pandemic had lower revenues.

The right panel of Figure 9 shows the median first-year revenues for necessity and opportunity firms founded in each year. The median among necessity firms is consistently lower than the median among opportunity firms started in the same year. However, that difference was smaller for firms founded around the Great Recession and the pandemic. Although median revenues among necessity firms showed some variance related to the business cycle, the first-year revenues across the cohorts were relatively more stable than across opportunity firms. This suggests that the types of firms opportunity entrepreneurs start may be more sensitive to market conditions than the ones necessity entrepreneurs open.

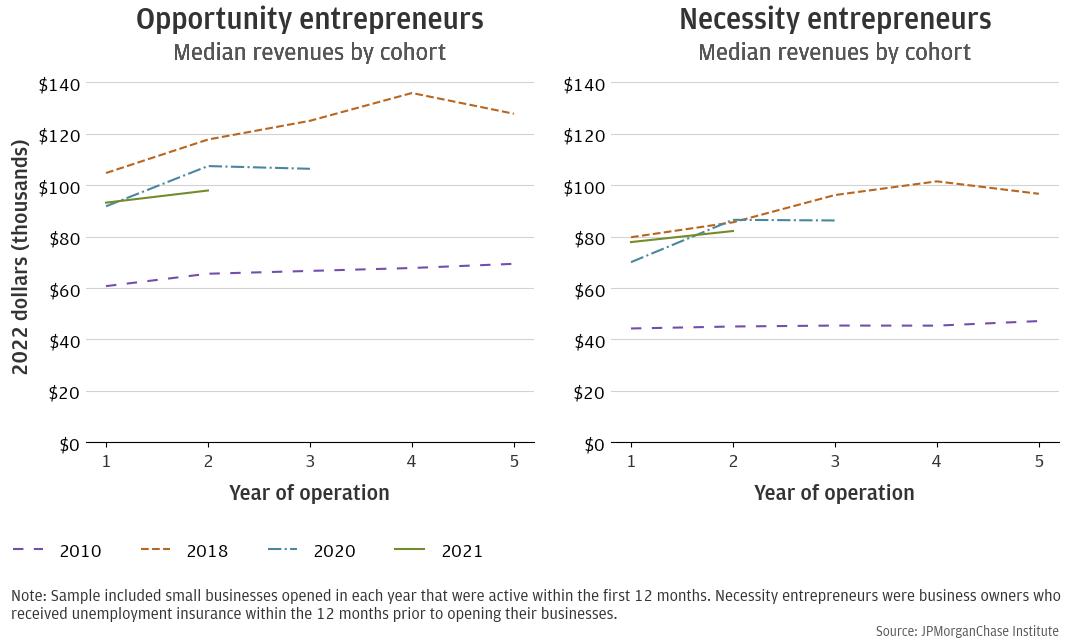

Necessity firms start smaller, and their revenues do not catch up to their counterparts founded by opportunity entrepreneurs over time. Figure 10 shows the median revenues of four cohorts of firms founded by opportunity entrepreneurs (on the left panel) and necessity entrepreneurs (on the right panel). The 2010 cohort represents firms founded around the Great Recession, with necessity entrepreneurs likely receiving UI in 2009-2010, during a time of high unemployment. Firms started by both necessity and opportunity firms in 2010 have shown little real growth in revenues during the first five years.

The 2018 cohort of firms were founded during a time of relatively favorable economic conditions, and the 2020-2021 cohorts consist of businesses started during the pandemic. These necessity firms followed similar revenue trajectories: the second-year revenues for the three cohorts were each in the $80,000-90,000 range. However, none of the median necessity firms caught up to their opportunity counterparts in the subsequent years.

Some of the differences between median revenues of firms founded by necessity and opportunity entrepreneurs may be due to different industry compositions, as discussed in Finding 1. We used a regression model of first-year revenues to control for observable firm and owner demographics. In addition to an indicator variable for UI receipt, the model also included controls for state, industry, and start year. The owner demographic variables included owner race, gender, age group, and personal deposit account balances prior to firm’s opening. Details are shown in the Appendix.

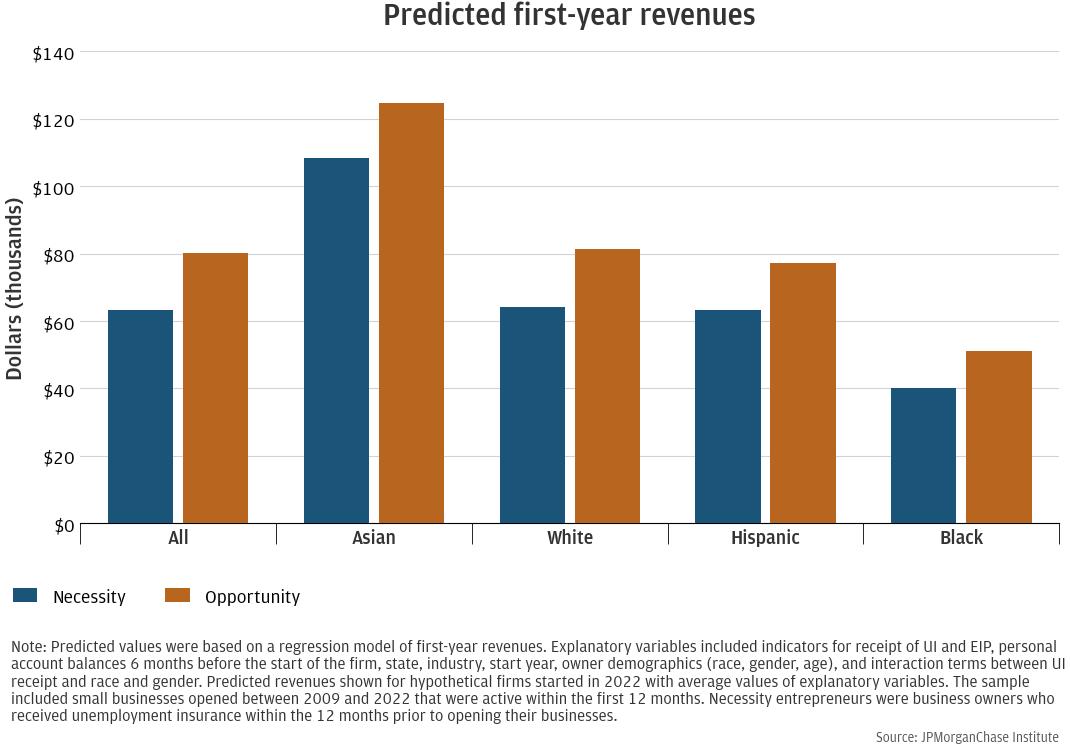

Using the coefficients from this model, we estimated the first-year revenues for necessity and opportunity firms assuming that the other observable variables were identical. Figure 11 displays the predicted first-year revenues for firms founded by necessity and opportunity entrepreneurs, holding other variables constant. The difference between necessity and opportunity firms appears smaller than the difference between their medians shown in Figure 10, suggesting that part of the reason firms started by necessity entrepreneurs are smaller than their opportunity counterparts was due to the types of firms they founded. However, observable firm characteristics did not fully account for the revenue gap between the two types of founders.

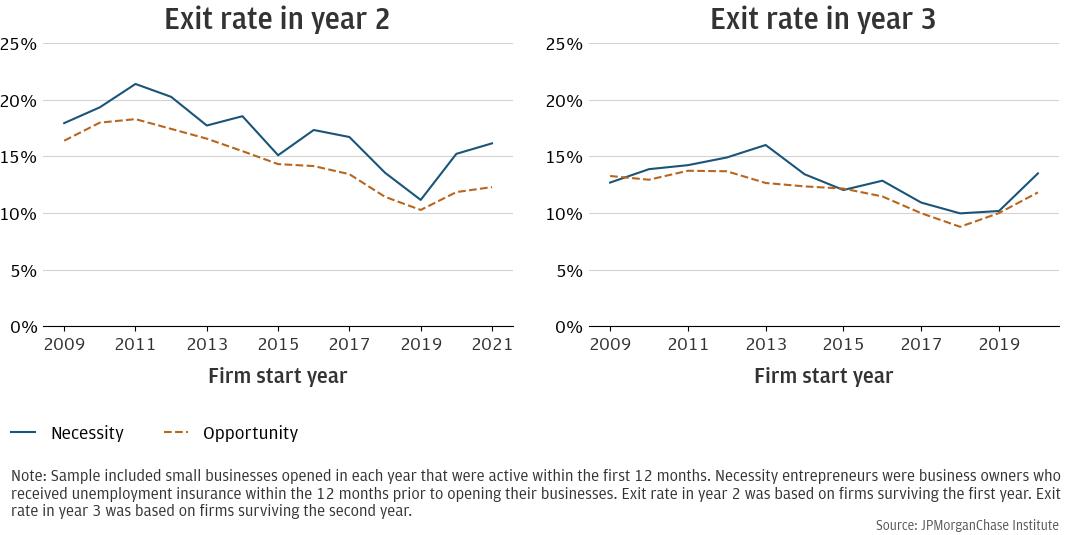

Not all new businesses survive, and that is part of the churn that constitutes business dynamism in the economy, contributing to innovation. Exit rates are typically higher when firms are young (Fairlie, et al. 2023). In addition, firms founded by necessity entrepreneurs are more likely to exit in early years, relative to ones founded by opportunity entrepreneurs, although the difference narrowed in the third year. Observable variation in firm characteristics, such as industry, can account for some of this difference. However, Black necessity entrepreneurs were materially more likely to exit relative to Black opportunity entrepreneurs even after controlling for firm characteristics.

Figure 12 shows the exit rates in the second and third years for firms founded by necessity and opportunity entrepreneurs. By construction, all firms in our sample survived the first year. For a given cohort (e.g., firms founded in 2018), the share of firms exiting in the second year was generally higher than the share exiting in the third year, conditional on surviving the second year.

Second year exit rates trended slightly downward over time: less than 15 percent of opportunity firms started in 2017 exited in their second year of operations, compared to over 15 percent of those started in 2009. Firms founded in 2018-2019 had noticeably lower second-year exit rates, but confounding circumstances make this difficult to interpret. Their second year of operations was 2020-2021, during the first two years of the pandemic. During this time, an unprecedented amount of small business support (e.g., the Paycheck Protection Program (PPP) and Economic Injury Disaster Loans (EIDL)) may have kept firms afloat. Moreover, even nonoperating firms may have deferred closing their bank accounts during the public health emergency.21 The exit rates for subsequent cohorts—firms founded in 2020-2021—were similar to those of pre-2018 cohorts, which may indicate a return to the historical trend.

For each cohort of firms starting in the same year, those founded by necessity entrepreneurs generally exited at higher rates than their counterparts founded by opportunity entrepreneurs. This difference narrowed in the third year, suggesting some convergence among the firms that survive the initial years.

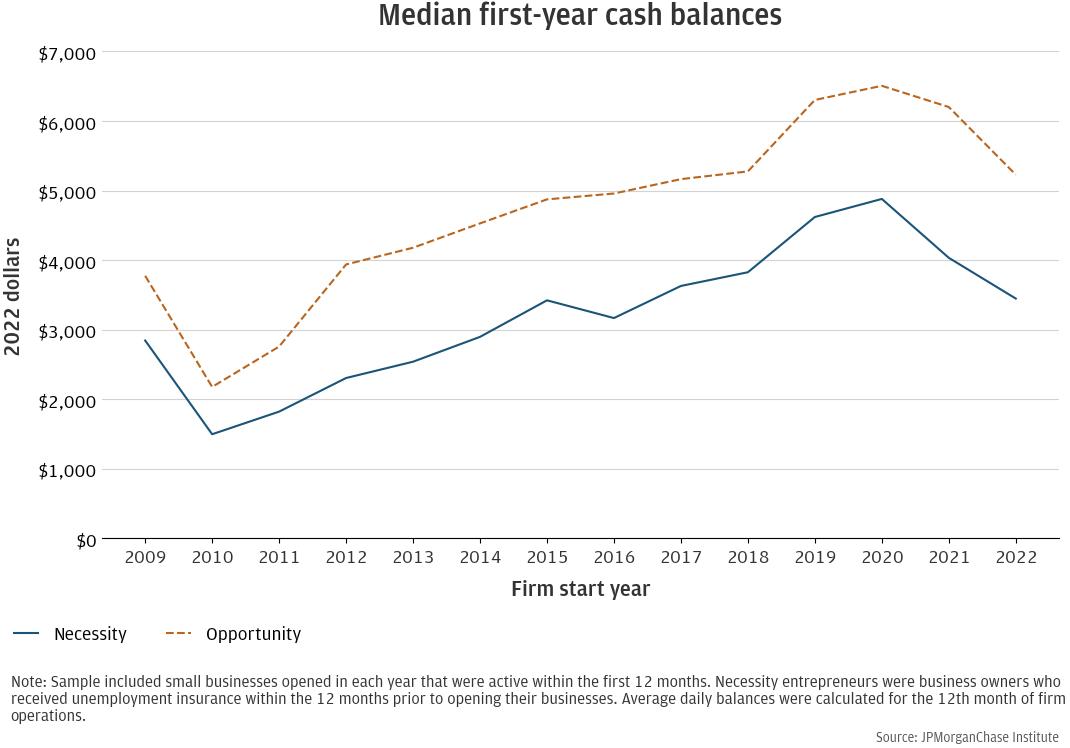

It may not be surprising that firms founded by necessity entrepreneurs exited at higher rates. First, they had lower cash balances, which suggests fewer financial resources upon which to draw. Figure 13 shows the median balances22 of each group of firms one year after the firm was founded. For every cohort, there was a material difference in cash balances between necessity and opportunity firms. For example, among necessity firms started in 2021, cash balances were about $4,000, compared to about $6,000 among opportunity firms.

This difference may have been exacerbated by the economic conditions of the time. The necessity firms founded in 2021 were founded by entrepreneurs who were unemployed in the previous year. Although they received unemployment insurance, which may have included supplemental unemployment insurance payments, their personal circumstances were likely worse off than those of opportunity entrepreneurs. In prior research, we noted that entrepreneurs with higher personal cash balances before starting their businesses also founded firms with higher balances (Wheat, Mac, and Tremper 2022), and cash buffers were positively correlated to firm survival (Farrell, Wheat, and Mac 2020c).

Second, even if necessity firms had access to the same resources, we might still expect them to have higher exit rates than opportunity firms. Necessity entrepreneurs were previously engaged in wage employment before involuntary unemployment, and they may prefer to return to wage employment when labor market conditions improve.

Necessity entrepreneurs start different kinds of firms from their opportunity counterparts. Their revenues and cash balances are lower, and the mix of industries varies over time. Such firm characteristics are correlated with firm exit. To control for observable differences between firms founded by necessity and opportunity entrepreneurs, we estimated a regression model of firm exits in their second year.

In addition to firm and owner characteristics, we included macroeconomic variables that summarized the labor market conditions after each firm’s first year. The unemployment rate, quits rate, and job openings rate are indicators of the alternatives entrepreneurs could pursue in wage employment.

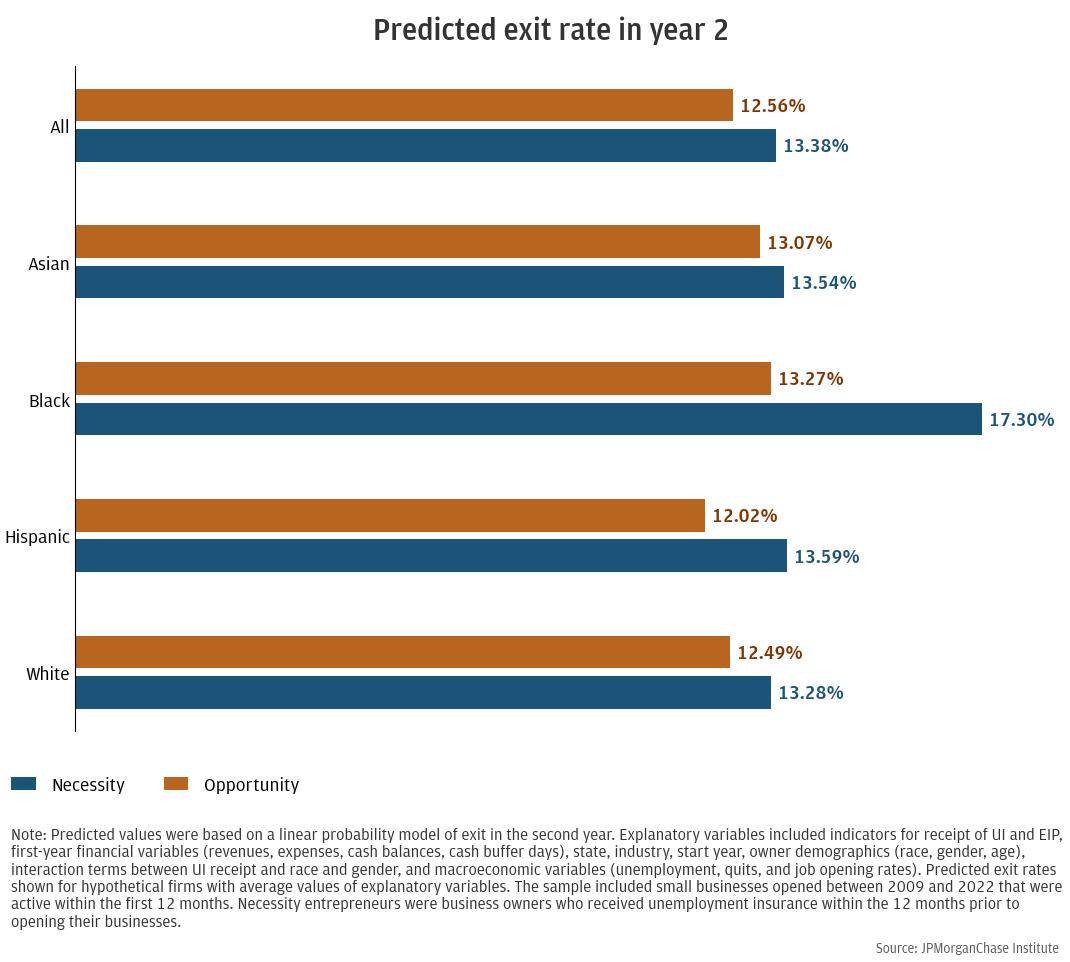

Figure 14 shows the predicted second year exit rates for necessity and opportunity entrepreneurs of different owner demographics, holding firm characteristics and macroeconomic variables constant. Necessity firms exited at higher rates than opportunity firms, but for most demographic groups, the difference was narrower than those shown in Figure 12. This suggests that much of the difference in exit rates was due to firm characteristics. However, the consistently higher exit rates for necessity entrepreneurs also suggests that they may prefer wage employment and choose to exit self-employment when possible. The difference in predicted exit rates is largest among Black business owners, which could imply that Black necessity entrepreneurs have stronger preferences for wage employment or reflect another unobservable factor.

Among opportunity firms, the differences in exit rates based on owner demographics was relatively small once firm characteristics was controlled for. This is consistent with past research (Farrell, Wheat, and Mac 2020c).

Firms founded by necessity entrepreneurs are more likely to exit within the first few years, compared to those founded by opportunity entrepreneurs. Some of those differences are due to the types of firms necessity entrepreneurs start, which typically have lower revenues and cash balances. However, differences in estimated exit rates persist even after controlling for firm characteristics and labor market conditions, suggesting that necessity entrepreneurs may prefer wage employment over self-employment.

Small businesses are a heterogeneous population, and efforts to segment this population can provide insights into not only the needs and challenges of each segment but also their growth trajectories (Farrell, Wheat, and Mac 2018). In this report, we focused on the circumstances under which entrepreneurs start their businesses, which may include their personal experiences with unemployment as well as general economic downturns. We offer the following implications of our findings:

Sample construction

Our sample included over 880,000 firms that opened Business Banking deposit accounts between 2009 and 2022. Our inclusion criteria are designed to ensure that the new business accounts likely represent active small businesses without excluding businesses that might be seasonal or have irregular cash flows. To be included in our sample, firms must have at least 10 transactions and $500 in outflows in at least three months of the first 12 months. They have at most two deposit accounts at a given time and operate in one of the 12 industries that are characteristic of the small business sector: construction, health care services, metals and machinery manufacturing, real estate, repair and maintenance, restaurants, retail, personal services, other professional services, wholesalers, high-tech manufacturing, and high-tech services.

Firms in our sample also have at least one owner who was the primary account holder of a personal Chase deposit account during the 12 months prior to the opening of the business account. This requirement allowed us to search for evidence of UI and identify likely necessity entrepreneurs. See Box 1 for details. We did not apply any activity requirements for the personal accounts.

For firms with more than one owner with available demographic information, we used the demographics of the oldest owner. Self-identified and modeled demographic data was obtained in 2021 from a third party for the JPMorganChase Institute to conduct economic research examining financial outcomes by race, ethnicity, and gender. The demographic data was matched to internal banking records using encrypted quasi-identifiers. This de-identified file that contains banking records and demographics is only available to the JPMorganChase Institute.

Regression models

Business outcomes are influenced by many factors, some of which may be related to industry or economic conditions and others that result from actions of the owners. We used multivariate regression models to estimate relationships between explanatory variables and two outcome variables, first-year revenues and the probability of exit in the second year. The models were estimated using ordinary least squares (OLS), and the coefficients were used to predict revenues or exit probabilities for hypothetical firms. This allowed us to compare the predicted outcomes of necessity and opportunity entrepreneurs while keeping the other variables constant.

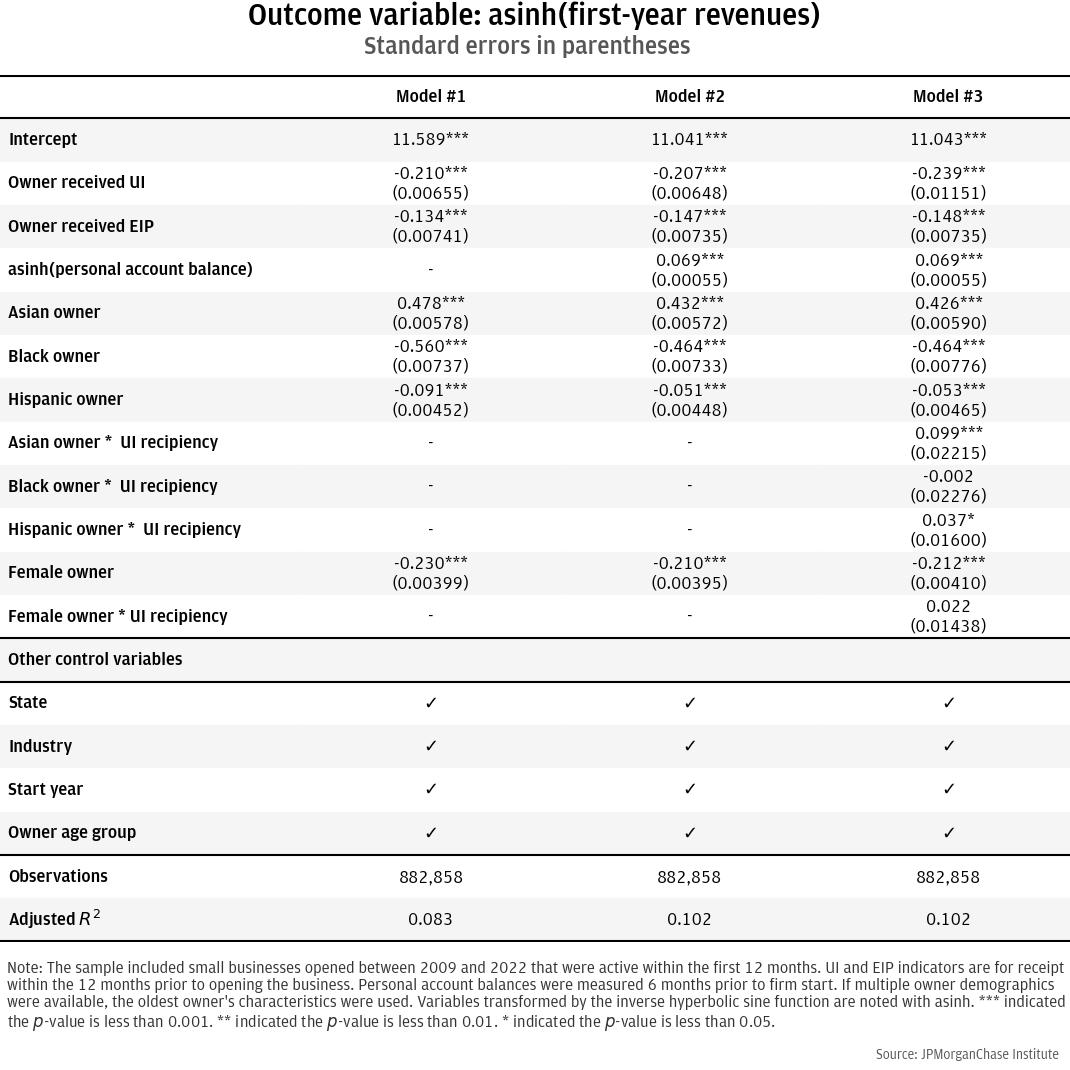

Table A1 shows the results from several specifications of regression models estimating first-year revenues. The dependent variable was transformed using the inverse hyperbolic sine function. The main explanatory variable of interest is an indicator for receipt of UI in the year prior to firm start. Across all models, the coefficient for this variable was negative and statistically significant, implying that necessity entrepreneurs start firms with lower revenues, all else equal. In Model #3, which includes the full set of control variables, the coefficient on UI receipt is –0.239, implying that firms founded by necessity entrepreneurs earned revenues that were 21 percent lower than those founded by opportunity entrepreneurs.23

Also included in our model is an indicator for receipt of any Economic Impact Payments (EIP) prior to the starting the business. Our results suggest that EIP had a negative effect on revenues, which may be surprising, as having additional funds could have helped entrepreneurs launch larger businesses. However, we would urge caution in interpreting this coefficient because EIP was only available during the pandemic. During that time, those who did not receive EIP had incomes too high to qualify.

Another variable that is intended to control for available personal resources is the personal account balance of the owner 6 months prior to firm start. As expected, there was a positive correlation between personal balances and first-year revenues, consistent with past research (Wheat, Mac, and Tremper 2022). The remaining explanatory variables include controls for state, industry, owner demographics (race, gender, age group), as well as interactions with UI receipt.

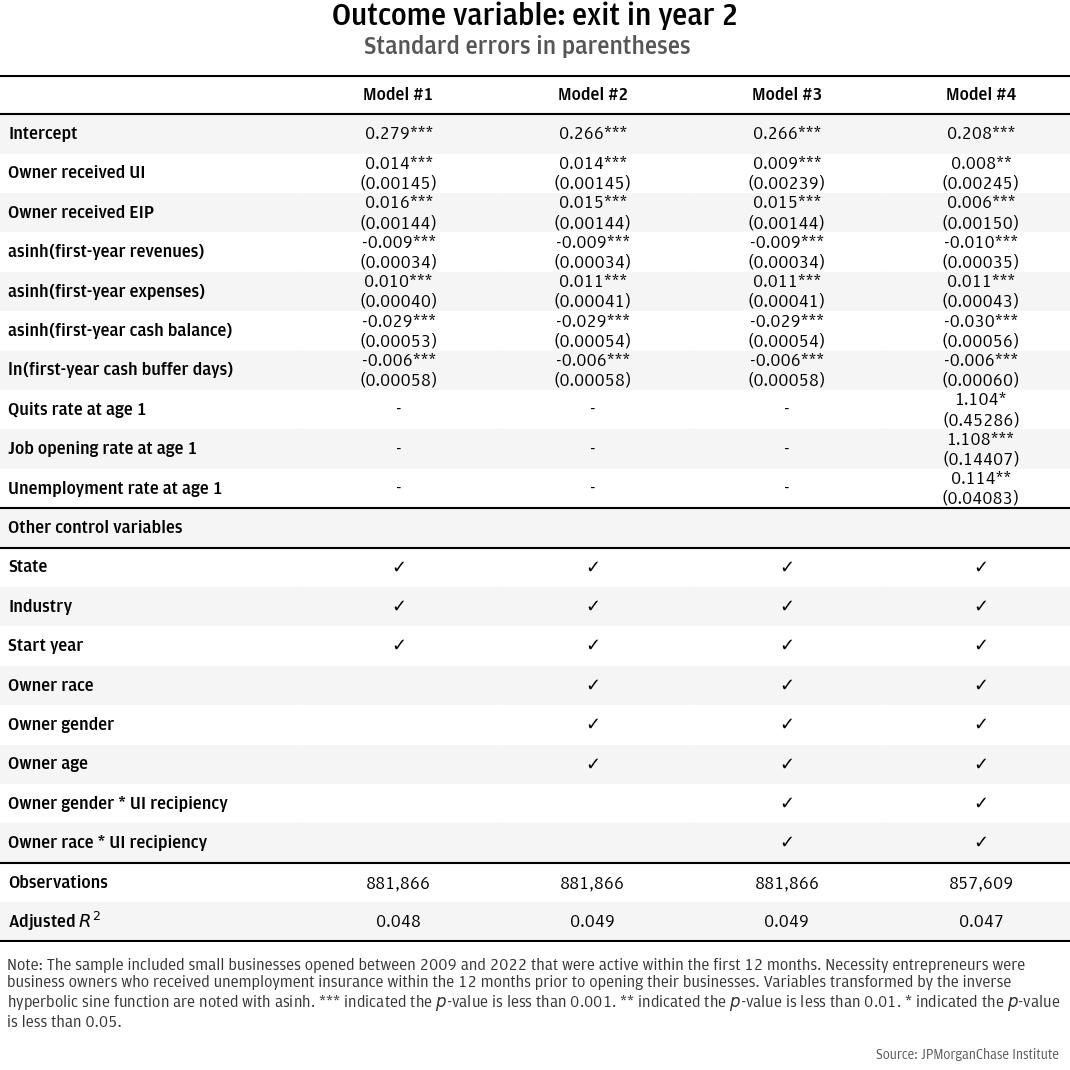

Table A2 shows the estimates from several linear probability models of firm exit in year 2. By construction, all firms in our sample survived their first year. Necessity entrepreneurs—those that received UI in the year prior to starting their businesses—were about 1 percentage point more likely to exit in their second year, depending on the model specification. Firms with higher revenues and cash balances were less likely to exit, and firms with higher expenses were more likely to do so.

Macroeconomic variables included the quits, job openings, and unemployment rates in the economy measured at each firm’s one year mark. The coefficient on the job opening rate is positive and the most statistically significant of the three, consistent with more entrepreneurs exiting when jobs are more available. An increase of 1 percentage point (or 0.01) in the job opening rate was associated with about a 1 percentage point increase in the probability of exit. New business owners, especially if they were necessity entrepreneurs, may prefer to return to wage employment when labor market conditions are favorable.

Bellemare, Marc F. and Casey J. Wichman. 2020. “Elasticities and the Inverse Hyperbolic Sine Transformation.” Oxford Bulletin of Economics and Statistics, 82(1).

Cunningham, Evan. 2018. “Great Recession, great recovery? Trends from the Current Population Survey.” U.S. Bureau of Labor Statistics. Monthly Labor Review. https://www.bls.gov/opub/mlr/2018/article/great-recession-great-recovery.htm

Decker, Ryan A., John Haltiwanger, Ron S. Jarmin, and Javier Miranda. 2016. “Declining Business Dynamism: Implications for Productivity?” https://www.brookings.edu/wp-content/uploads/2016/08/haltiwanger_conference_draft.pdf

Decker, Ryan A. and John Haltiwanger. 2022. “Surging Business Formation in the Pandemic: Causes and Consequences.” https://www.bostonfed.org/-/media/Documents/events/2022/labor-markets/papers/surging-business-formation-in-the-pandemic-causes-and-consequences-haltiwanger-decker.pdf

Ewing Maron Kauffman Foundation. 2022. “Who is the Entrepreneur? New Entrepreneurs in the United States, 1996-2021.” Trends in Entrepreneurship. Kansas City, Missouri.

Fairlie, Robert W. 2013. “Entrepreneurship, Economic Conditions, and the Great Recession.” Journal of Economics and Management Strategy, Volume 22, Number 2, 207-231.

Fairlie, Robert W. 2022. “National Report on Early-Stage Entrepreneurship in the United States: 2021.” Kauffman Indicators of Entrepreneurship, Ewing Marion Kauffman Foundation: Kansas City.

Fairlie, Robert W. and Frank M. Fossen. 2019. “Defining Opportunity versus Necessity Entrepreneurship: Two Components of Business Creation. NBER Working Paper 26377. https://www.nber.org/system/files/working_papers/w26377/w26377.pdf

Fairlie, Robert W., Zachary Kroff, Javier Miranda, and Nikolas Zolas. 2023. The Promise and Peril of Entrepreneurship: Job Creation and Survival among US Startups. The MIT Press.

Falk, Gene, Jameson A. Carter, Isaac A. Nicchitta, Emma C. Nyhof, and Paul D. Romero. 2021. “Unemployment Rates During the COVID-19 Pandemic: In Brief.” Congressional Research Service. https://crsreports.congress.gov/product/pdf/R/R46554/9

Farrell, Diana, Christopher Wheat, and Chi Mac. 2018. “Growth, Vitality, and Cash Flows: High-Frequency Evidence from 1 Million Small Businesses.” JPMorganChase Institute. https://www.jpmorganchase.com/content/dam/jpmc/jpmorgan-chase-and-co/institute/pdf/institute-growth-vitality-cash-flows.pdf.

Farrell, Diana, Christopher Wheat, and Chi Mac. 2020a. “Small Business Financial Outcomes during the Onset of COVID-19.” JPMorganChase Institute. https://www.jpmorganchase.com/institute/all-topics/business-growth-and-entrepreneurship/small-business-financial-outcomes-during-the-onset-of-covid-19.

Farrell, Diana, Christopher Wheat, and Chi Mac. 2020b. “Small Business Financial Outcomes during the COVID-19 Pandemic.” JPMorganChase Institute. https://www.jpmorganchase.com/institute/all-topics/business-growth-and-entrepreneurship/report-small-business-financial-outcomes-during-the-covid-19-pandemic.

Farrell, Diana, Christopher Wheat, and Chi Mac. 2020c. “Small Business Owner Race, Liquidity, and Survival.” JPMorganChase Institute. https://www.jpmorganchase.com/institute/research/small-business/report-small-business-owner-race-liquidity-survival.

Fikri, Kenan and Daniel Newman. 2024. “Business Applications Eked Out a New Record in 2023.” Economic Innovation Group. https://eig.org/2023-business-formation/.

Ganong, Peter, Fiona Greig, Pascal Noel, Daniel M. Sullivan, and Joseph Vavra. 2021. “Micro and Macro Disincentive Effects of Expanded Unemployment Benefits.” JPMorganChase Institute. https://www.jpmorganchase.com/content/dam/jpmc/jpmorgan-chase-and-co/institute/pdf/when-unemployment-insurance-benefits-are-rolled-back-paper.pdf.

Misera, Lucas and Emily Ryder Perlmeter. 2023. “2023 Report on Startup Firms Owned by People of Color: Findings from the 2022 Small Business Credit Survey.” Small Business Credit Survey. Federal Reserve Banks. https://doi.org/10.55350/sbcs-20230616.

Nichols, Austin and Margaret Simms. 2012. “Racial and Ethnic Differences in Receipt of Unemployment Insurance Benefits during the Great Recession.” Urban Institute.

Schweitzer, Mark E. and Scott Shane. 2016. “The Ins and Outs of Self-Employment: An Estimate of Business Cycle and Trend Effects.” Federal Reserve Bank of Cleveland, Working Paper No. 16-21. https://doi.org/10.26509/frbc-wp-201621.

Storey, D.J. 1991. “The Birth of New Firms—Does Unemployment Matter? A Review of the Evidence.” Small Business Economics 3, 167-178.

Wheat, Chris, Chi Mac, and Nicholas Tremper. 2022. “Small Business Owner Liquid Wealth at Firm Startup and Exit.” JPMorganChase Institute. https://www.jpmorganchase.com/institute/all-topics/business-growth-and-entrepreneurship/small-business-ownership-liquid-wealth-startup-exit.

Wheat, Chris, James Duguid, Lindsay E. Relihan, and Bryan Kim. 2021. “The COVID Shock to Online Retail: The persistence of new online shopping habits and implications for the future of cities.” JPMorganChase Institute. https://www.jpmorganchase.com/institute/all-topics/community-development/covid-shock-to-online-retail.

Whittaker, Julie M. and Katelin P. Isaacs. 2022. “Unemployment Insurance (UI) Benefits: Permanent-Law Programs and the COVID-19 Pandemic Response.” Congressional Research Service. https://crsreports.congress.gov/product/pdf/R/R46687.

We thank Karmen Hutchinson and Man Xu for their hard work and vital contributions to this research. Additionally, we thank Oscar Cruz, Annabel Jouard, and Alfonso Zenteno for their support. We are indebted to our internal partners and colleagues, who support delivery of our agenda in a myriad of ways and acknowledge their contributions to each and all releases.

We would like to acknowledge Jamie Dimon, CEO of JPMorgan Chase & Co., for his vision and leadership in establishing the Institute and enabling the ongoing research agenda. We remain deeply grateful to Peter Scher, Vice Chairman; Tim Berry, Head of Corporate Responsibility; Heather Higginbottom, Head of Research, Policy, and Insights and others across the firm for the resources and support to pioneer a new approach to contribute to global economic analysis and insight.

This material is a product of JPMorganChase Institute and is provided to you solely for general information purposes. Unless otherwise specifically stated, any views or opinions expressed herein are solely those of the authors listed and may differ from the views and opinions expressed by J.P. Morgan Securities LLC (JPMS) Research Department or other departments or divisions of JPMorgan Chase & Co. or its affiliates. This material is not a product of the Research Department of JPMS. Information has been obtained from sources believed to be reliable, but JPMorgan Chase & Co. or its affiliates and/or subsidiaries (collectively J.P. Morgan) do not warrant its completeness or accuracy. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. No representation or warranty should be made with regard to any computations, graphs, tables, diagrams or commentary in this material, which is provided for illustration/reference purposes only. The data relied on for this report are based on past transactions and may not be indicative of future results. J.P. Morgan assumes no duty to update any information in this material in the event that such information changes. The opinion herein should not be construed as an individual recommendation for any particular client and is not intended as advice or recommendations of particular securities, financial instruments, or strategies for a particular client. This material does not constitute a solicitation or offer in any jurisdiction where such a solicitation is unlawful.

Wheat, Chris and Chi Mac. 2024. “When opportunity knocks: How economic cycles shape entrepreneurial ventures and their success.” JPMorganChase Institute. https://www.jpmorganchase.com/institute/all-topics/business-growth-and-entrepreneurship/when-opportunity-knocks-how-economic-cycles-shape-entrepreneurial-ventures-and-their-success.

Footnotes

The Census Bureau’s Business Application Series is available through https://fred.stlouisfed.org/series/BABATOTALSAUS.

The personal account need not remain open after the business account is opened.

See Fairlie and Fossen (2019) for a list of recent examples of researchers using the necessity and opportunity entrepreneurship framework. Other researchers have used the concepts of “push” and “pull” entrepreneurship to convey similar distinctions (Storey 1991).

We leveraged prior work in identifying UI benefit payments in transaction data (Ganong, et al. 2021).

The Department of Labor notes that while each state sets its own eligibility guidelines for UI benefits, a typical qualification is to be “unemployed through no fault of your own” (https://www.dol.gov/general/topic/unemployment-insurance).

For example, Illinois recommends direct deposit of UI benefits, but paper checks are also an option. Debit cards were previously an option until late 2021 (https://ides.illinois.gov/unemployment/payment-methods.html).

The Kauffman Foundation’s rate of new entrepreneurs measures the percent of the population that starts a new business, using data from the Current Population Survey (CPS). In 2020, it was 0.38 percent, compared to 0.31 percent in 2019. In 2009, it was 0.34 percent

(https://indicators.kauffman.org/indicator/rate-of-new-entrepreneurs).

The U.S. Census Bureau’s Business Application Series tracks business applications for tax IDs as indicated by applications for an Employer Identification Number (EIN) through filings of the IRS Form SS-4 (https://www.census.gov/econ/bfs/current/index.html).

The Census Bureau’s Business Application Series is available through https://fred.stlouisfed.org/series/BABATOTALSAUS.

Based on the National Bureau of Economic Research’s (NBER) determination of U.S. business cycles

(https://www.nber.org/research/data/us-business-cycle-expansions-and-contractions).

U.S. Department of Labor UI Data Summary (https://oui.doleta.gov/unemploy/data_summary/definitions.pdf).

The Kauffman indicators are based on data from the U.S. Census Bureau’s Current Population Survey (CPS), using the survey questions about unemployment and an empirical approach proposed by Fairlie and Fossen (2019). Although the CPS includes a question asking respondents if they quit their job, Fairlie and Fossen do not exclude voluntary unemployment from their measure of necessity entrepreneurs to facilitate comparisons across datasets. Many datasets do not offer this distinction

(https://indicators.kauffman.org/indicator/opportunity-share-of-new-entrepreneurs/).

Based on the unemployment rate from the CPS for food services and drinking places

(https://data.bls.gov/timeseries/LNU04034262).

Based on the unemployment rate from the CPS for personal and laundry services (https://data.bls.gov/timeseries/LNU04034273).

Non-store retail includes electronic shopping and mail-order houses, vending machine operators, and other direct selling establishments.

The CARES Act created a temporary benefit of $600 per week that supplemented most weekly UI benefits; the benefits were available from March 29, 2020 through July 25, 2020. Subsequent legislation reestablished the benefit at the lower amount of $300 per week, effective during parts of 2021 (Whittaker and Isaacs 2022).

The rate of new entrepreneurs was defined as the percent of individuals who do not own a business in the first survey month and start a business in the following month with 15 or more hours worked per week (Fairlie 2022).

We use account closure as a proxy for firm closure.

Each firm’s average daily balance was calculated for its twelfth month of operations, and the median among each group is shown.

We used an approximation for interpreting the percentage change in the outcome variable transformed with the inverse hyperbolic sine function (revenues) associated with a change in the indicator variable (receipt of UI) proposed by Bellemare and Wichman (2020): exp(b – 0.5 Var(b)) – 1, where b is the estimated coefficient of interest.

Authors

Chris Wheat

President, JPMorganChase Institute

Chi Mac

Business Research Director